Florida Homeowners Insurance Crisis 2026:

Over 1 Million Homes Uninsured — What Every Buyer Needs to Know

How fraud drove Florida insurance to 3–5x the national average, what the 2022–2023 reforms changed,

and why your agent’s approach to insurance can make or break your home purchase.

By Eric Konoski | Broker Associate & Team Lead, K&C Group at eXp Realty

SRES® & SFR® Certified | Retired NYPD Captain

Published February 2026 | Last Updated February 2026

Sarasota, Charlotte, Manatee & Lee Counties • Southwest Florida

KEY TAKEAWAYS — What You Need to Know • Over 1 million Florida homes (1 in 5) are currently uninsured • Systemic Assignment of Benefits (AOB) fraud—not hurricanes—drove premiums to $6,000–$15,000/year • 2022–2023 legislative reforms eliminated AOB and one-way attorney fees • Insurance lawsuit volumes have dropped 60%+; Citizens Insurance proposed its first rate cut in a decade (~11%) • Buyers can reduce costs through elevation certificates (20–30% flood savings), impact windows (84.6% ROI + insurance discounts), and wind mitigation inspections • Insurance is now the second-largest homeownership cost in Florida—your agent should evaluate it before you write an offer, not at closing |

How Many Florida Homes Are Uninsured in 2026?

As of 2026, over one million Florida homes are uninsured—approximately one in every five residential properties in the state. Many of these homeowners are uninsured not by choice: some cannot obtain coverage due to the age or condition of their property (particularly roofs over 15 years old), and others have been priced out as annual premiums reached $6,000 to $15,000 in coastal areas of Southwest Florida.

This crisis is not a background statistic—it is actively reshaping every real estate transaction in Sarasota, Charlotte, Manatee, and Lee Counties. Buyers routinely discover, sometimes 20 to 25 days into a contract, that insurance costs make their dream home unaffordable. Deals collapse. Or worse: buyers close and end up house poor because nobody ran the real numbers before they committed.

At K&C Group, we treat this as unacceptable. We analyze the insurance profile of every property because the difference between an agent who opens doors and one who protects your financial future starts with understanding the numbers.

Why Is Florida Homeowners Insurance So Expensive?

Florida homeowners insurance became the most expensive in the nation primarily due to systemic Assignment of Benefits (AOB) fraud—not because of hurricane damage alone. According to legislative findings, Florida accounted for just 9% of the nation’s homeowners insurance claims but generated 79% of all homeowners insurance lawsuits. The vast majority of these lawsuits stemmed from fraudulent and inflated contractor claims enabled by the state’s AOB laws.

How the Assignment of Benefits (AOB) Scam Worked

The fraud followed a consistent pattern. Contractors—often going door-to-door unsolicited—told homeowners they needed a new roof, or that they could get one “at no cost.” The homeowner would sign an Assignment of Benefits, transferring their insurance claim rights to the contractor. The contractor would then perform approximately $8,000 worth of work and submit a bill to the insurance company for $30,000 or more.

When the insurer refused to pay the inflated amount, the contractor would file a lawsuit. Under Florida’s one-way attorney fee statute, the contractor faced zero financial risk: if they won, the insurance company paid the claim plus all attorney fees. If they lost, the contractor owed nothing. This created a systematic incentive to file bogus claims, and the volume was staggering.

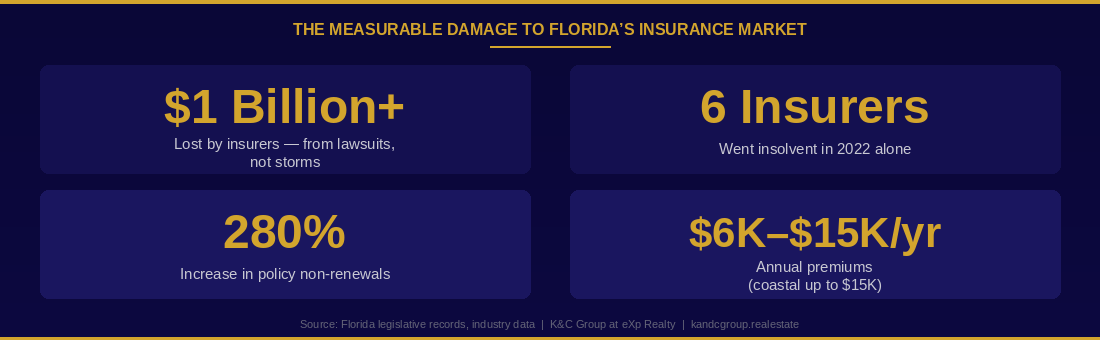

The Measurable Damage to Florida’s Insurance Market

The result was catastrophic for the broader market: insurers lost over a billion dollars from litigation (not natural disasters), six carriers went insolvent in 2022, non-renewals jumped 280%, and premiums for Florida homeowners reached approximately $6,000 on average—with coastal and waterfront properties facing $11,000 to $15,000 annually. These costs were driven by litigation, not weather.

At K&C Group, our approach is built on evidence, not assumptions. When we evaluate a property for clients, we analyze the full insurance profile—roof age, hurricane protection, flood zone, elevation—because these factors directly impact what you’ll actually pay each month. That’s the difference between a transaction-focused agent and a fiduciary.

Did Florida Insurance Reform Work? 2022–2023 Results and Rate Reductions

Yes. Florida’s 2022–2023 insurance reforms have produced measurable results. Lawsuit volumes dropped over 60% following the legislative changes, with an additional 25% decline through the first half of 2025. Citizens Property Insurance Corporation—Florida’s state-backed insurer of last resort—proposed its first rate cut in over a decade, approximately 11%. Multiple private carriers have also filed rate decreases.

What the Reforms Changed

- Eliminated Assignment of Benefits on new policies. Homeowners can no longer sign over claim rights to contractors, closing the primary mechanism for inflated and fraudulent claims.

- Removed one-way attorney fees. Contractors who sue insurers now face financial risk if they lose, eliminating the incentive for frivolous litigation.

- Reduced litigation volumes dramatically. Insurance-related lawsuits in Florida have dropped by more than 60% since the reforms took effect, with continued declines through 2025.

The market has not fully corrected—Florida insurance premiums remain three to five times the national average—but the trajectory has clearly shifted. For buyers considering Southwest Florida, this represents meaningful progress and a stabilizing market environment.

| We track these legislative and market shifts closely so our clients don’t have to. Schedule a complimentary consultation at kandcgroup.realestate or call (727) 255-1690. |

How to Reduce Homeowners Insurance Costs When Buying in Florida

Florida home buyers can reduce insurance costs through several proven strategies: obtaining an elevation certificate (which can lower flood insurance by 20–30% or more), purchasing homes with impact windows or hurricane shutters, ensuring the roof is under 15 years old, getting a wind mitigation inspection to document premium-reducing construction features, and evaluating FEMA flood zone designations before making an offer. The most important step, however, is working with an agent who evaluates insurance as part of every property analysis—not as an afterthought after you’re under contract.

5 Insurance Factors Your Agent Should Evaluate Before You Make an Offer

Too many agents in Southwest Florida still don’t bring up insurance until their buyer is under contract. At K&C Group, we assess these five critical factors on every property showing:

- Roof Age and Condition. According to our Construction Cost Guide, roof replacement for a standard 2,400 sq ft Florida home costs $10,800–$48,000 depending on material (asphalt shingles, metal, or tile). Roofs over 15 years old may be uninsurable in Florida, making this a deal-breaker—not a negotiation point.

- Hurricane Protection. Impact windows deliver approximately 84.6% ROI according to our CMA Improvement Value Guide and provide permanent, invisible storm protection with meaningful insurance premium discounts. Hurricane shutters provide lower returns (50–70% ROI) but still offer protection. No hurricane protection significantly increases insurance costs.

- FEMA Flood Zone Designation. Flood zone classification directly determines whether flood insurance is required and at what cost. Out-of-state buyers are often unaware of how dramatically this impacts total ownership cost in Florida.

- Elevation Certificate. An elevation certificate documents how far above the base flood elevation a property sits. This single document can reduce flood insurance premiums by 20–30% or more, yet most buyers skip it because it’s not included in a standard survey and their agent doesn’t mention it.

- Wind Mitigation Features. A wind mitigation inspection documents construction features—such as roof-to-wall connections, secondary water resistance, and opening protection—that qualify for windstorm insurance discounts. This inspection is inexpensive relative to the savings it can unlock.

What Is the True Monthly Cost of Owning a Home in Florida?

The true monthly cost of owning a home in Florida includes the mortgage payment, homeowners insurance ($500–$1,250/month in Southwest Florida), flood insurance (varies by zone and elevation), property taxes (approximately 1–2% of home value annually), HOA fees (if applicable), and maintenance/utilities ($150–$400+/month). For a typical Soutwest Florida-area home, insurance alone can add $500 to $1,250 per month to the cost that many buyers don’t fully account for when determining affordability.

This is critical because what a mortgage lender approves and what a buyer can comfortably afford are frequently two different numbers. Many first-time buyers—and even experienced buyers relocating from states with lower insurance costs—go into homeownership without understanding the complete monthly obligation. The result is they become house poor: they can make the payment, but they’re financially strained every month.

A responsible buyer’s agent calculates the complete monthly cost before the offer, not after. At K&C Group, we build a full cost-of-ownership analysis for every property our clients consider, ensuring there are no surprises at closing or after.

Insurance-Smart Home Buying Checklist for Southwest Florida

Before making an offer on any property in Sarasota, Charlotte, Manatee, or Lee County, the following items should be completed or scheduled:

- Roof age and condition verified — Roofs over 15 years may be uninsurable. Replacement costs: $10,800–$48,000 (source: K&C Group Construction Cost Guide v4.2).

- Hurricane protection assessed — Impact windows (84.6% ROI, insurance discounts) vs. shutters (50–70% ROI) vs. no protection (significant premium risk).

- FEMA flood zone identified — Determines flood insurance requirements and cost before you commit.

- Insurance quotes obtained during due diligence — Not at closing. During inspections, alongside your home inspection and appraisal.

- Elevation certificate requested — Can reduce flood insurance by 20–30%+. Not included in standard surveys.

- Wind mitigation inspection scheduled — Documents features qualifying for windstorm insurance discounts. Low cost, high return.

- Complete monthly cost calculated — Mortgage + homeowners insurance + flood insurance + taxes + HOA + maintenance. The real number, not just the mortgage payment.

At K&C Group, this checklist is our standard operating procedure for every client, every property. We believe you deserve to know exactly what you’re buying—not just what it looks like from the curb.

Frequently Asked Questions: Florida Homeowners Insurance

The following questions are among the most common we hear from buyers considering Southwest Florida.

How much does homeowners insurance cost in Florida in 2026?

As of early 2026, the average annual homeowners insurance premium in Florida is approximately $6,000. However, costs vary significantly by location and property characteristics. Inland Sarasota properties may see premiums in the $3,500–$6,000 range, while coastal and waterfront homes in Sarasota, Charlotte, and Lee Counties can face $11,000 to $15,000 or more annually. These figures do not include flood insurance, which is an additional cost for properties in FEMA-designated flood zones.

Why is Florida homeowners insurance so much more expensive than other states?

Florida homeowners insurance is three to five times the national average primarily because of systemic Assignment of Benefits (AOB) fraud that plagued the state for years. Florida had only 9% of national homeowners insurance claims but generated 79% of the lawsuits. Insurers lost over $1 billion from litigation, six carriers went insolvent in 2022, and the costs were passed to policyholders. Legislative reforms in 2022–2023 have significantly reduced fraud-driven litigation, and rate reductions are beginning to take effect.

Are Florida insurance rates going down in 2026?

Yes, Florida insurance rates are beginning to decline for the first time in years. Citizens Property Insurance Corporation has proposed an approximately 11% rate reduction—its first in over a decade. Several private carriers have also filed rate decreases. Insurance lawsuit volumes have dropped more than 60% since the 2022–2023 reforms, with an additional 25% decline through the first half of 2025. While premiums remain elevated compared to national averages, the market trajectory is clearly improving.

What is an elevation certificate and how does it reduce flood insurance in Florida?

An elevation certificate is a document prepared by a licensed surveyor that shows how many feet above the base flood elevation (BFE) a property sits. Homes with higher elevations relative to the BFE qualify for significantly lower flood insurance premiums—reductions of 20–30% or more are common. Elevation certificates are not included in a standard property survey and must be specifically requested. Many buyers skip this step because their agent doesn’t mention it, potentially costing thousands of dollars per year in unnecessary flood insurance premiums.

Do impact windows reduce insurance costs in Florida?

Yes. Impact windows provide permanent hurricane protection and typically qualify homeowners for meaningful windstorm insurance premium reductions. According to K&C Group’s CMA Improvement Value Guide, impact windows deliver approximately 84.6% ROI in the Sarasota market, making them the gold standard for hurricane protection. Unlike shutters, impact windows require no deployment before a storm and provide continuous protection. Full-house impact window installation for a Southwest Florida home typically adds $12,000–$45,000 in value depending on the property tier.

How old can a roof be and still get insurance in Florida?

In Florida, roofs over 15 years old may be uninsurable or face significantly restricted coverage options. Many insurance carriers will not write new policies for homes with roofs exceeding this age, and existing policyholders may face non-renewal without passing a roof inspection verifying at least 5 years of life left on the roof. A roof replacement in Southwest Florida costs approximately $10,800–$20,400 for asphalt shingles, $19,200–$36,000 for metal, and $19,200–$48,000 for concrete or clay tile on a standard 2,400 square foot home (source: K&C Group Construction Cost Guide v4.2). Roof age should be verified before making an offer on any Florida property, as it directly impacts both insurability and purchase negotiations.

What should I look for in a real estate agent when buying in Florida?

When buying a home in Florida, look for an agent who evaluates insurance costs and insurability before you write an offer, not after you’re under contract. Your agent should assess roof age, hurricane protection (impact windows vs. shutters), FEMA flood zone designations, and wind mitigation features as part of every property showing. They should obtain insurance quotes during your due diligence period and calculate the complete monthly cost of ownership—including mortgage, insurance, flood insurance, taxes, HOA, and maintenance—before you commit. An agent who only talks about finishes and curb appeal without addressing these financial factors is not acting as your fiduciary.

Work With a Southwest Florida Real Estate Team That Understands the Numbers

The Florida insurance landscape is complex—but it’s not something you have to navigate alone. The reforms are working. Rates are beginning to decline. And with the right strategy and representation, Southwest Florida remains one of the most compelling places in the country to buy a home.

But you need an agent who treats insurance as a core part of every transaction, who runs the numbers before you commit, and who ensures you understand the complete cost of ownership before you sign anything.

That’s what we do at K&C Group. Founded by retired NYPD Captain Eric Konoski, and real estate professional Nicholle Clint, our team brings a disciplined, investigative approach to every transaction across Sarasota, Charlotte, Manatee, and Lee Counties. We don’t just sell homes—we protect our clients’ investments with precision, evidence, and transparency.

SCHEDULE YOUR COMPLIMENTARY CONSULTATION Whether you’re relocating to Southwest Florida, selling your home, buying your first home, or investing in the market, we’ll walk you through the numbers so you can make a confident, informed decision. Call Today! ☎ (941) 352-9041 Serving Sarasota, Charlotte, Manatee & Lee Counties Because Every Move Matters. |

ABOUT THE AUTHOR

Eric Konoski is Team Lead and Broker Associate for K&C Group at eXp Realty, serving Southwest Florida’s Sarasota, Charlotte, Manatee, and Lee Counties. A retired NYPD Captain, Eric brings a data-driven, investigative approach to real estate. He holds the Seniors Real Estate Specialist (SRES®) and Short Sales and Foreclosure Resource (SFR®) certifications. Eric founded K&C Group with Nicholle Clint on the principles of precision, evidence-based analysis, and client protection.

Disclaimer: This article is provided for informational and educational purposes only and does not constitute financial, legal, or insurance advice. Insurance rates, regulations, and availability are subject to change. Always consult with licensed insurance professionals for specific coverage questions. Statistics and data referenced are from publicly available legislative records, industry reports, and K&C Group’s proprietary research as of February 2026. K&C Group at eXp Realty.